Economic Reset Under The Powell Doctrine | QPOL Issue #48

How Powell’s monetary policy is resetting economic metrics and putting power back into the hands of the market.

As the fight for the debt ceiling drags on, Powell’s hawkish monetary policy continues to work its magic in the background. Albeit he’s basing his decisions off lagging economic data presented to him by his less than favorable staff, it’s clear his policy is having a direct effect on the economy by destroying demand and sailing the US economy seemingly closer to a popularly mocked “soft landing” and reaching the Fed’s goal of a 2% inflation target.

Meanwhile, Fed policy seems to be simultaneously resetting the rules and putting power back into the hands of market participants. Danielle DiMartino Booth has been on the media circuit covering excellent ground on what’s been happening based on the Fed’s policy and where things could go from here, and how we got in this situation in the first place.

I took the time to identify some key aspects from some of her recent media appearances. From there I formulated the hypothesis that Powell’s policy is in fact not only working, but is resetting the board game of who controls the economy: the oligarchs, or the market?

The Market Is Doing The Fed’s Job

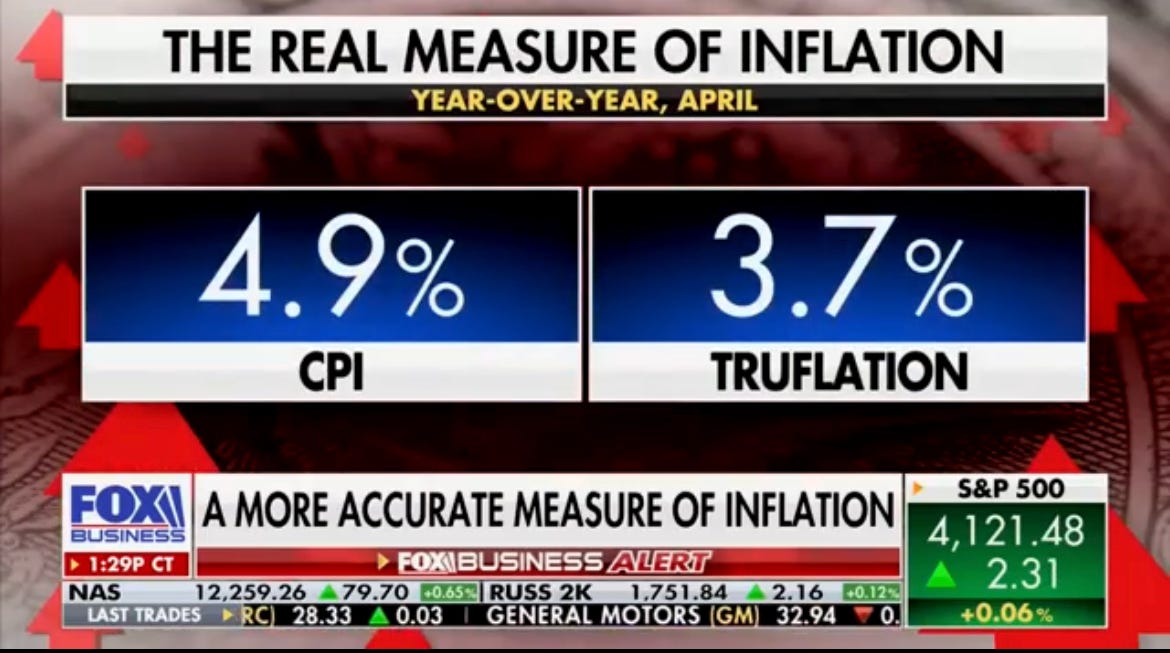

Inflation came in at 4.9%.

Obviously, this is much more appealing than the expected reports of 5% or 5.1%. It’s also closer to the Fed’s 2% goal compared to last year when the US was at 10%.

This just goes to show that despite the lag in Powell’s monetary policy, it’s effective nonetheless in bringing inflation down (botched metrics or not) and the Fed’s balance sheet keeps decreasing by the billions on weekly basis. Due to this lag in CPI (more on this later) statisticians are scrambling to catch up.

Even if the Fed were to pause rates, decreasing the balance sheet could continue until the end of 2023. Decreasing the balance sheet is in its own right, a form of continued tightening monetary policy because as collateralize loans against treasuries are fully serviced, the debt is therefore paid off. That is why loans by definition are deflationary.

The balance sheet continues to decrease in the background (quantitative tightening/QT) during a serious situation in banking where customers keep pulling their deposits. Where are those deposits going you might ask? Why, in higher yielding money market funds that pay 5% and up. Thanks to the Fed’s high interest rate policy, people’s deposits are capitalizing money markets without the need for an over leveraged economy under ZIRP.

Booth also explains this as an example of Powell’s vision of a parallel policy where credit crunches become a form of synthetic tightening (according Monday’s loan officer report that came back as “stale”) or the inability for consumers and businesses alike to access credit. This hindered access to credit is its own form of tightening even if it’s not considered a rate hike/decreasing the balance sheet. Under a Powell Doctrine free of ZIRP, the markets are simply doing the Fed’s job for them.

No Contagion In Sight

As of now, Booth sees no systemic risk to contagion, at least we haven’t seen anything global in nature like how Lehman assets affected the Landis Banks in Germany (Landis banks simply refer to the smaller German banking sector).

Contagion may be slow even if one bank fails after the other because it doesn’t cause a cascading effect. Why? Because that are most vulnerable are those that benefited from and took the most advantage of ZIRP and SF-based monetary policy (SVB et.al). AKA, the most degenerate and over leveraged.

SVB failed because they kept operating as if Powell was going to pivot back to the Zero Bound because their business was only possible thanks to ZIRP and loose, irresponsible monetary policy of the San Francisco Fed under the legacy of Yellen.

Implications of the US defaulting on the debt from nations that hold huge amounts of US debt (Japan and China) may stoke fears of these nations selling treasuries. Historically this isn’t the case. When the US defaulted in 2011 and US sovereign debt was downgraded, US treasuries were still viewed as the global safe haven and nations flooded into them. The same thing could very well happen again because there’s no safe-haven substitute for a reserve currency other than the dollar.

So the selling of treasuries may not be an issue, but what is problematic is the selling of equities because the market has been so over-leveraged, especially since the last couple years of cheap debt and stimulus after COVID. Again, the market has been in denial about Powell not going back to the zero bound and ending the Fed Put.

A Case For True Metrics

Truflation on the other hand came in at 3.7%.

What is Truflation you might ask? Simply put, it’s a more accurate measurement to calculate inflation based on real-time market data.

Truflation was created by traders in response to the lag in typical inflation reports. Their jobs can’t rely on lagged data from CPI. Truflation by contrast is based on 24/7 real-time market activity and is dynamic based what traders are following day-to-day.

In my eyes, this is the equivalent of SOFR for calculating inflation. Just as SOFR is a collateralized interest rate indexed to money market deals, it’s based off real market activity. New metrics like SOFR and Truflation may be signposts that reveal the Fed’s goal of bringing back true price discovery in the market (more on this later).

The Rise and Fall of the Bernanke Doctrine

When rates were zero, Private Equity set monetary policy as the rest of Wall Street followed in their footsteps. Booth covers this in detail on her recent appearance on Vivek Ramaswamy’s podcast.

The lending regulations under Dodd Frank made it so bankers could no longer run their operations like hedge funds. With banks being put on this new tight leash, entrepreneurs needed to get their money elsewhere.

Booth describes the “brain drain” in banking as bankers packed up and moved their Wild West operations into private equity and the shadow banking system instead. There, they could write their own rules with a new Venture Capital rebrand, provide cheap credit to entrepreneurs (with their own cheap credit) that headed “unicorn companies” and leverage themselves to the hilt under ZIRP.

All of this was only possible with the Bernanke Doctrine. As Booth describes, it was the “original sin” of the Fed by asserting that the repurchasing of assets on the Fed’s balance sheet (quantitative easing/QE) was only possible if rates were at the zero bound. ZIRP handed over monetary policy to PE. Now with a Fed under Powell, PE (especially over leveraged PE), is finally being punished as rates grow North of 5% and assets are being properly repriced.

Make Price Discovery Great Again

Price discovery can’t be found in the market place without higher rates. ZIRP distorted the economy under the Bernanke Doctrine. Now, Powell has been designated to unwind the damaged mentality that’s plagued the consciousness of the market that money is free. That’s why Fed governors are so hawkishly vocal about “not being done”with their policy. It’s about getting the Fed’s monetary independence back and correcting asset prices.

As the superiority of the shadow banking system is being challenged, this is also enabling deals to be made by other institutions and participants where before they were hindered by ZIRP.

Booth covers it in the last 7 minutes of this Blockworks interview.

As rates increased, assets that banks purchased under Dodd Frank that were deemed as “safe” depreciated. Now, that’s changed as deals are being made while price discovery can finally take place. In my recent interview with Tom Luongo, we broke down exactly how such a deal could take place.

QPOL 009 - Tom Luongo: Dare To Be Wrong!

Listen now (118 min) | Tom joins the show to discuss the banking and pension crisis, how prices are being reset and deals will be made to restore the US financial system, dogs, nuclear war, the culture war, George Carlin, and Tom hates the Stones… 😭 ~ Phil Gibson If you enjoy the content, consider supporting my work for less than what a blue check mark on twitter costs you… …

Let’s Make A Deal!

For example, take a regional bank and a pension fund.

Under current circumstances, the bank:

can’t loan (at least not as liberally)

has depreciated assets thanks to rate hikes

needs cash or something to fill the holes on its balance sheet, especially when they’re needing to pay out attractive rates to their clients’ saving accounts

The pension:

needs yield and duration to pay out their clients

can then buy the discounted assets from the bank (say a CRE loan for a tractor supply shop at a 15% discount from $100k)

that asset could pay roughly 6%-7% and the pension has the cash flow to pay out their clients

The banks now have the cash to go by newly issued treasuries that pay ~ 5% and up to fill the holes on their balance sheet.

This is just one example. Hell, even the PE firms leveraged to the hilt might have a chance of survival.

Multiply this process by the countless businesses and financial institutions in the market place. The possibilities for deals are endless. This is only possible when rates aren’t at the zero bound distorting prices, and the shadow banks don’t have a monopoly over deals. Now, proper price discovery can finally be conducted in the marketplace.

No ZIRP.

No systemic contagion.

No Fed bailout necessary.

To risk overstating it, Powell doesn’t need to bail out the banks. He’ll leave that to the pensions. The banks get cash as pensions get their yield, meaning boomers get their social security. This is a massive transfer of wealth from ZIRP leaches like BlackRock who get screwed, back to the middle class.

Let The Chips Fall

This could all be a sign of Powell’s vision of putting economic policy back in the hands of the market. We’re witnessing these changes in real time. You may not be able to trust Powell, but what you can trust are his and the primary dealers’ incentives to survive.

For markets, especially in this fiat-driven world, it’s all a confidence game. More importantly, it’s information warfare. That’s all markets and prices are, information depicting our emotions. Therefore, markets move off sentiment Headlines drive that sentiment. But, who controls the headlines?

Call them Davos, or whatever secret society placeholder of your choosing, but it’s ultimately oligarchical vandals selling out the American economy and undermining our financial system. This is precisely what we’re up against. The regional banking crisis is a self-fulfilled prophecy and myth concocted as propaganda by the oligarch class who both architected and benefited the most from ZIRP to force Powell back to the zero bound.

For what it’s worth, dear reader, I’d like to share an anecdote with you if I may. What I’ve personally heard by people who work at regional banks is that they have plenty of reserves secured at their designated Fed branch. This “crisis” is pure propaganda and a hit-job on the American banking sector by vandals within it who are working against us. The truth is the majority of banks are fine.

Some will win. Some will lose. Some are born to sing the blues. In an economy under the Powell Doctrine, he’s letting the chips rightfully fall where they may…

~ Phil Gibson

If you enjoy the content, consider supporting my work for less than what a blue check mark on twitter costs you… :-)

For more insights and musings, follow me on Twitter @MrPseu

For business inquires, contact heyQPOL@gmail.com

Tip Me on CashApp/Bitcoin:

bc1qhlqefvm3f6mc33k7shgzns299wsgzc9jd9puxs

| A guest post by

|