The Fed Implements a Central Bank Digital Currency | QPOL Issue #21

The Fed's real motives for a CBDC.

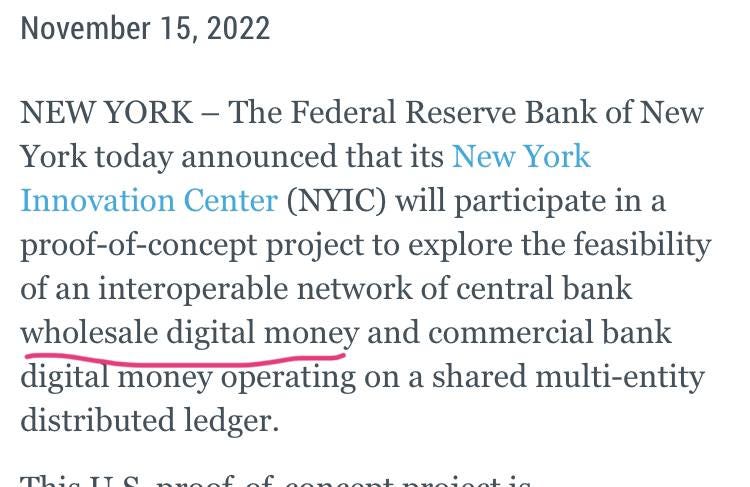

On Tuesday November 15, the Federal Reserve Bank of New York announced a 12-week pilot program for a digital dollar. This had the internet all up in a traumatic frenzy of fear as rumors spread of the possible of a government Central Bank Digital Currency (CBDC).

There are many reasons to fear such a program being implemented. It’s been done in China via apps like What’sApp and WeChat where people’s entire lives are on a financial app which dictates their social credit scores based on their spending habits and what they post on social media. In fact, CNBC’s Ryan Browne even reported as of February 2022,

…the PBOC's digital yuan comes with a number of problems that make it less attractive in Western countries. Critics say it's too centralized and could be used to boost government surveillance. That's because, unlike cash, people's digital transactions can be tracked online.

Thankfully, this pilot by the Fed and participating commercial banks is not a project for such a digital panopticon dystopia.

The following article features the announcement of the pilot straight from the NY Fed’s website that briefly describes the program and its intentions. Though vague in some areas, it is clear what their objectives are.

The key phrase here is wholesale. It’s crucial to understand the difference between the two types of CBDCs - wholesale & retail.

A wholesale CBDC system uses blockchain for payment & settlement between banks.

A retail CBDC system uses blockchain for payments at a customer-facing level. This type of CBDC presents the dystopian concerns many have about CBDC that can use smart contracts to program specific capital controls on individuals

With some clarity on the definitions at play here, we cam now understand what the Fed will be testing and why.

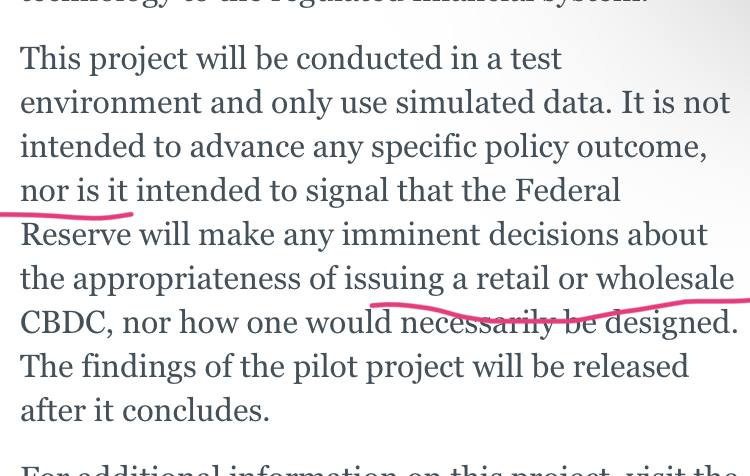

“This U.S. proof-of-concept project is experimenting with the concept of a regulated liability network. It will test the technical feasibility, legal viability, and business applicability of distributed ledger technology to settle the liabilities of regulated financial institutions through the transfer of central bank liabilities.”

Notice, “settle the liabilities of regulated financial institutions through the transfer of central bank liabilities,” meaning that this tech is for the banks use only. This is what would be considered a wholesale CBDC. The current legacy rails used by commercial banks and central banks is archaic and slow, and has been well overdue for an upgrade. This system would optimize the settlement of reserve assets between banks in an updated and robust fashion finally fit for the 21st. century.

From this passage, although vague, it’s quite unlikely the Fed would be working on a retail CBDC, as they have no plans or “imminent decisions” to announce on the matter.

Central Bank Bait & Switch

Now knowing what the goals of the Fed are, who’s to say they won’t just bait and switch American citizens into using a retail CBDC? Although anything is possible, the incentives of the banks don’t align with such an objective.

Simply put, based on who the banks are and what they’re here to do, it is not in their incenttive to implement a retail CBDC. Conceptually, in a world with retail CBDCs the banks aren’t even in the picture. To put it frankly, a retail CBDC would literally put the commercial banks out of business.

The commercial banking sector is the largest lobby in the world. A retail CBDC would force them to forfeit their power and monopoly of the creation of money, or private capital via issuing loans. A retail CBDC would remove them for the middlemen that they are, but would result in the end of banking and the creation of private capital and capitalism as we know it, and institute modern monetary theory.

As an American consumer, the relationship with you and your money would be from the Federal Reserve and straight to your pocket. Although this may sound more efficient, it opens up Pandora’s box for capital controls and totalitarianism none can begin to imagine.

Straight from the Horse’s Mouth

Don’t just take my word for it. In May of this year, credit union and banking trade groups released a joint letter to the chair and ranking member of the House Financial Services Committee, warning of the “devastating consequences” if the Federal Reserve moves forward with a Central Bank Digital Currency (CBDC).

“In effect, a CBDC will serve as an advantaged competitor to retail bank deposits that will move money away from banks and into accounts at the Federal Reserve where the funds cannot be lent back into the economy. These deposit accounts represent 71% of bank funding today. Losing this critical funding source would undermine the economics of the banking business model, severely restricting credit availability, increasing the cost of credit, and causing a slowdown of the economy. ABA estimates that even a CBDC where accounts were capped at $5,000 per ‘end user’ could result in $720 billion in deposits leaving the banking system.”

A retail CBDC is illogical for the commercial banks to implement. At the risk of sounding redundant, people must understand that there will be NO retail CBDC in the United States of America. The commercial banks will not forfeit the creation and preservation of private capital and the monetary transmission mechanism. It’s common sense. There won’t be a CBDC at the retail level where the commercial banks forfeit their power and we all get paid from the Fed into our bank app. I spoke about this extensively on a recent podcast with my friend and colleague Cory Tucek below.

As we saw in September, Jaime Dimon will not let this stand. A retail CBDC is lockstep with MMT and a climate-change focused monetary policy. These mandates would certainly “pave the road to hell for America.”

A RETAIL CBDC would mean the end of the creation of private capital via commercial banking/US sovereignty over monetary policy. This is clearly something the Fed is currently fighting to keep via raising rates/moving away from LIBOR to SOFR, and being America’s bank, not the globe’s. I have laid out extensively how and why raising rates as well as multiple monetary tools are destroying the creation of offshore dollars here for reference.

Despite the political pressure the banks and the Fed face, they are the ones in control of the purse strings of the global communists out of Davos and will stand tall to protect their industry, the creation of private capital, and the preservation of American capitalism.

One must be aware of the fear-porn and disinformation tactics being touted not only by the mainstream media, but even news outlets in the alternative news space. It is easy for us as humans to be overwhelmed by fear and uncertainty, but that’s exactly what the enemy wants. Aside from false-flags and nuclear war, fear mongering is the only tactic they have left to force us into submission. They are that desperate. Fortunately for us as free-thinking individuals, we have the truth on our side. Stay strong, alert, and use common sense. As a colleague of mine likes to say, don’t let the anxiety pimps get the best of you.

~ Phil Gibson