From Zero To Homeward Bound | QPOL Issue #44

From Zero To Homeward Bound | QPOL Issue #44

Reading between the lines of Dimon's annual letter to JPM shareholders.

While mindless wojacks on twitter cried last week about Jamie Dimon praising the ESG market in the JP Morgan annual letter to shareholders, the real meat was (though not surprisingly) overlooked.

In the letter, Dimon blamed regulators for the recent banking panics and warned the current crisis which will leave economic repercussions for years to come is nowhere close to being over. He noted the recent failure of 3 US banks and the rescue of Credit Suisse from the Swiss government challenges the public’s confidence in the banking industry and prompted investors to price in higher risk of recession in the US.

Dimon argued the banking failures were largely due to the regulations of Dodd Frank after the ‘08 credit crunch. Dodd Frank incentivized banks to fill their portfolios with treasury bonds which during a time of Zero Bound interest rates were very liquid and considered risk-free.

These regulations were concocted as if their authors couldn’t even fathom a world in which rates were anywhere North of zero. As we saw with the recent bank failures, the rise in rates put holes in the banks’ balance sheets as their treasury bonds fell in value. This resulted in the “bailout” with the Fed backstopping them and, in cooperation with the government, created the BTFP. In hindsight, these seemingly safe government securities turned out to be the exact opposite of safe.

As Danielle DiMartino Booth illustrates in her recent piece Too Small Not To Fail, banks were also incentivized to issue loans to commercial real estate (CRE), a sector that is currently taking a major hit as Powell continues his hawkish policy. Defaults on CRE loans could add to the blow of banks’ balance sheets even more so than treasuries because the Fed ain’t backstopping CRE since it doesn’t qualify at the Fed Window. This could be the real kicker that results in more bank casualties.

To add insult to injury, the Stress Tests that the Fed conducts on banks to determine their financial stability didn’t account for rate increases either. All things considered, it clearly seems like the regulations after the GFC were intentionally put in place to set the banking industry up for failure and to force the Fed to pivot in order to bail out any failing banks, leaving egg on the face of any Fed Chair who attempts to bring sanity and credibility back to US markets. Powell. It may be a stretch, but these regulations seem like Davos trip mines to pin Powell into a corner to keep rates at the Zero Bound. As DDB says, a Zero Bound world is a world without the Fed.

All this goes to show how in denial not only the markets, but the entire financial industry was about rate hikes ever happening. Commentators like Jeff Snider are still assuming this Fed is just like Greenspan’s Fed, and that the Eurodollar Futures Curve that’s still indexed to LIBOR (which is pretty much obsolete at this point), will be the market playing the strongman that forces the Fed to pivot. The numbers clearly say otherwise…

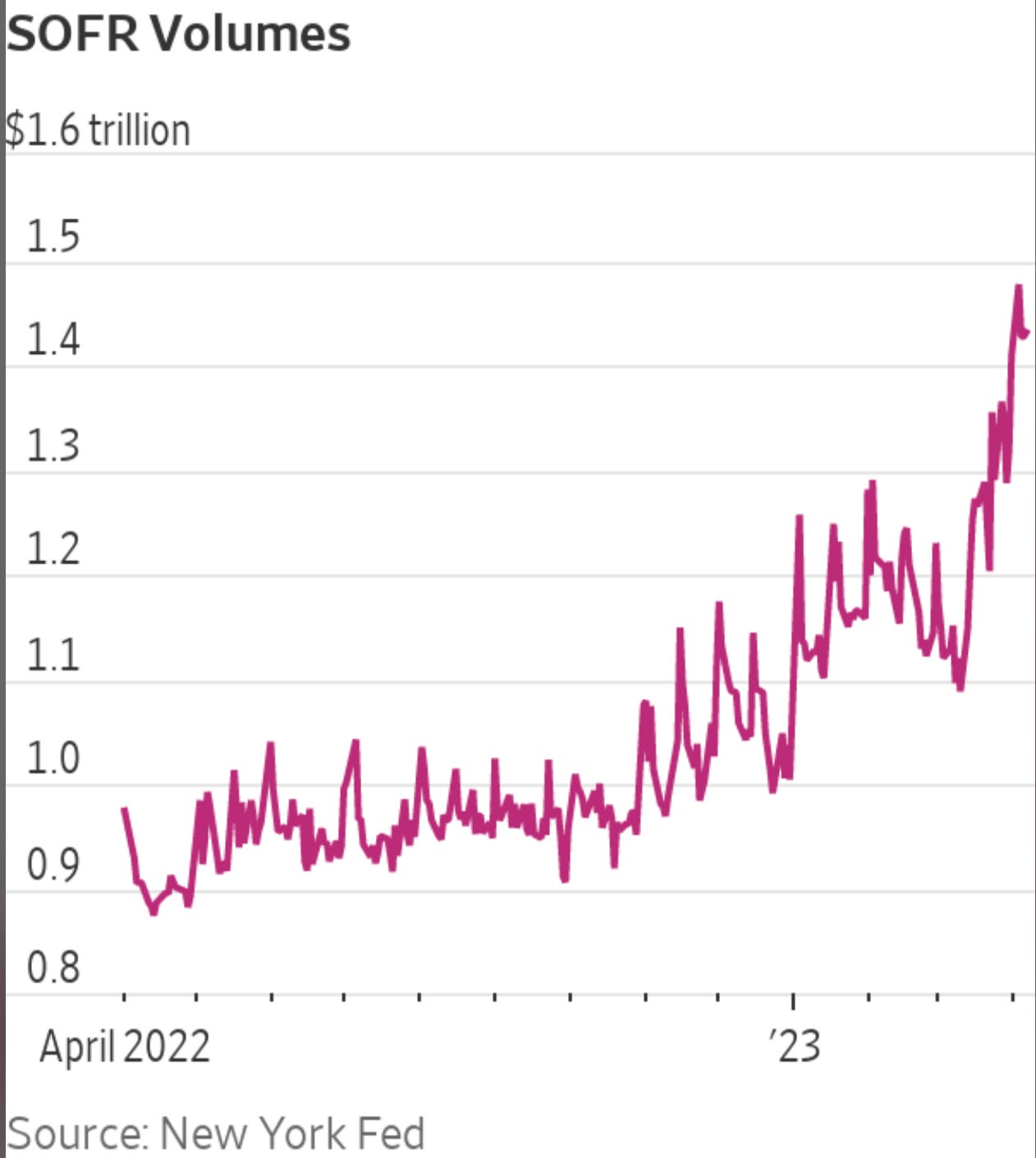

It makes sense why there’s been so much push-back against Powell’s monetary policy. But Zero Bound interest rates are not sustainable for any economy and Powell’s goal is to bring sanity back into markets by pricing in real risk and allowing the chips to fall where they may. AKA: ending the Fed put while pulling multiple levers of monetary policy such as SOFR and having primary dealers become involved in the private credit markets to further insulate the banking system. These are only a handful of strategies Powell has taken to declare US monetary independence.

All these happenings in monetary policy are rebounds from the Zero Bound. Just as LIBOR was the US’s ball and chain of monetary policy, Zero Bound is just a part of the chain link. Dimon was right to call it out in his letter because Zero Bound not only cripples the banking system, but cripples the economy. A crippling economy means a crippling banking sector. No matter how much leverage and free money gets printed in the system to inflate bubbles and makes people rich on paper, it’s not sustainable, and makes the US an unattractive place for investors to park their capital. What goes up must come down.

Thankfully, what this will ultimately mean is that the 1/5 of companies that are zombie companies will be demolished, bringing back some economic sanity and true price discovery to investors, while also creating deflation for the Fed. Yes, there will be pain, but who is that pain truly inflicted on? I’d argue Davos and the over-leveraged offshore dollar system. Without Zero Bound interest rates, such leverage wouldn’t have flowed into the US economy to cause the GFC in the first place. As economic sanity is realized in the US, that’s when capital flight from overseas will flood the DOW, safe haven assets like gold, Bitcoin, and US treasuries. That’s when you know we’ve gone from Zero to Homeward Bound, baby!

One might ask if Jamie Dimon is truly warning of economic pain, or cheering it on?

~ Phil Gibson

If you enjoy the content, consider supporting my work for less than what a blue check mark on twitter costs you… :-)

Thank you for reading QPOL. If you feel you’re getting value out of it, don’t be afraid to say the Quiet Parts Out Loud and share it with a friend. Please and thank you.

For more insights and musings, follow me on Twitter @MrPseu

For business inquires, contact heyQPOL@gmail.com

| A guest post by

|